Understanding Risk: How to Define Your Personal Risk Profile

Home > Understanding Risk: How to Define Your Personal Risk Profile

Home > Understanding Risk: How to Define Your Personal Risk Profile

👤 Ketan Jogalekar

In the world of investing, "risk" is often treated like a four-letter word. We’re taught to avoid it. But in reality, risk and return are two sides of the same coin. If you want your money to grow faster than inflation, you have to accept some level of uncertainty.

The secret isn't avoiding risk—it's managing it. To do that, you need to understand your personal Risk Profile.

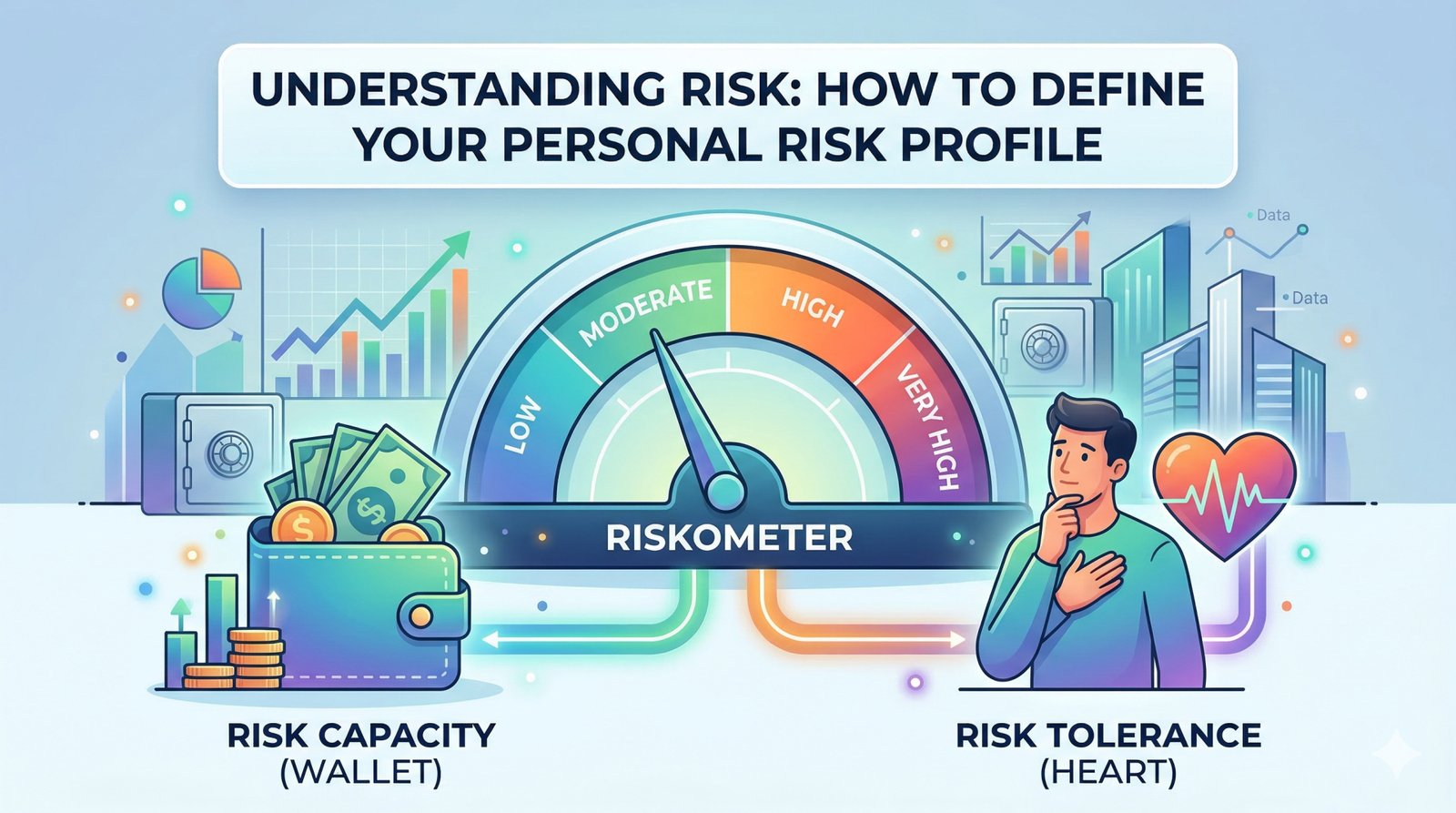

Your risk profile isn't just about how you feel when the market drops; it’s a combination of two very different factors: your Risk Tolerance and your Risk Capacity.

1. Risk Tolerance (The Heart)

This is your psychological ability to stomach market swings. If the stock market drops 10% in a week, do you stay calm and see it as a buying opportunity, or do you lose sleep and want to sell everything? Tolerance is emotional.

2. Risk Capacity (The Wallet)

This is your financial ability to take a hit. A 25-year-old with a steady job and no dependents has a high risk capacity. A 58-year-old nearing retirement with a daughter’s wedding next year has a low risk capacity. Even if the 58-year-old is "brave" (high tolerance), their financial situation (low capacity) means they shouldn't take big risks.

Most investors fall into one of these three buckets. Which one sounds like you?

Conservative: You prioritize the safety of your principal over high growth. You are okay with lower returns if it means your portfolio doesn't fluctuate much. (Best suited for: Debt funds, Liquid funds).

Moderate: You seek a balance. You want better-than-inflation growth but aren't comfortable with extreme "rollercoaster" swings. (Best suited for: Hybrid or Balanced Advantage funds).

Aggressive: You are focused on long-term wealth creation. You understand that markets will be volatile in the short term, but you are willing to ride those waves for the potential of high double-digit returns. (Best suited for: Equity funds, Mid-cap/Small-cap funds).

Whenever you look at a mutual fund at TruePath Invest, you’ll see a graphic called a Riskometer. This is a mandatory tool provided by SEBI to help you understand exactly what you’re getting into. It ranges from "Low" to "Very High."

Matching the fund’s Riskometer to your personal Risk Profile is the best way to ensure you don't end up in an investment that keeps you up at night.

The biggest risk of all is taking too little risk. If you keep all your money in a savings account because you're afraid of the market, you are guaranteeing that inflation will erode your wealth. The goal is to find the "Sweet Spot"—the level of risk that allows your money to grow while letting you sleep soundly.

Your risk profile changes as your life changes. A promotion, a new baby, or approaching retirement will all shift your capacity and tolerance. This week, ask yourself: If my portfolio dropped 20% tomorrow, would I be okay? If the answer is a hard "no," it’s time to re-evaluate your asset mix.

Next week, we look at another crucial variable: Time Horizon Matters: How Long You Plan to Invest Influences Your Strategy.

At TruePath Invest, we use professional risk-profiling tools to help you identify your comfort zone. We’ll make sure your portfolio matches your personality and your pocketbook.